Forget traditional practice valuations. Learn the only metric that matters: can you afford the loan payment? Plus the 5 valuation methods and 9 factors that actually determine price.

This is the question that keeps practice buyers awake at night. And I'm going to give you the clearest answer I can: affordability matters more than valuation.

I've walked into dozens of practices where brokers printed out valuations that look sophisticated. Multi-page reports with formulas and benchmarks and comparable sales. None of it matters if you can't actually afford the loan payment.

The One Rule That Matters

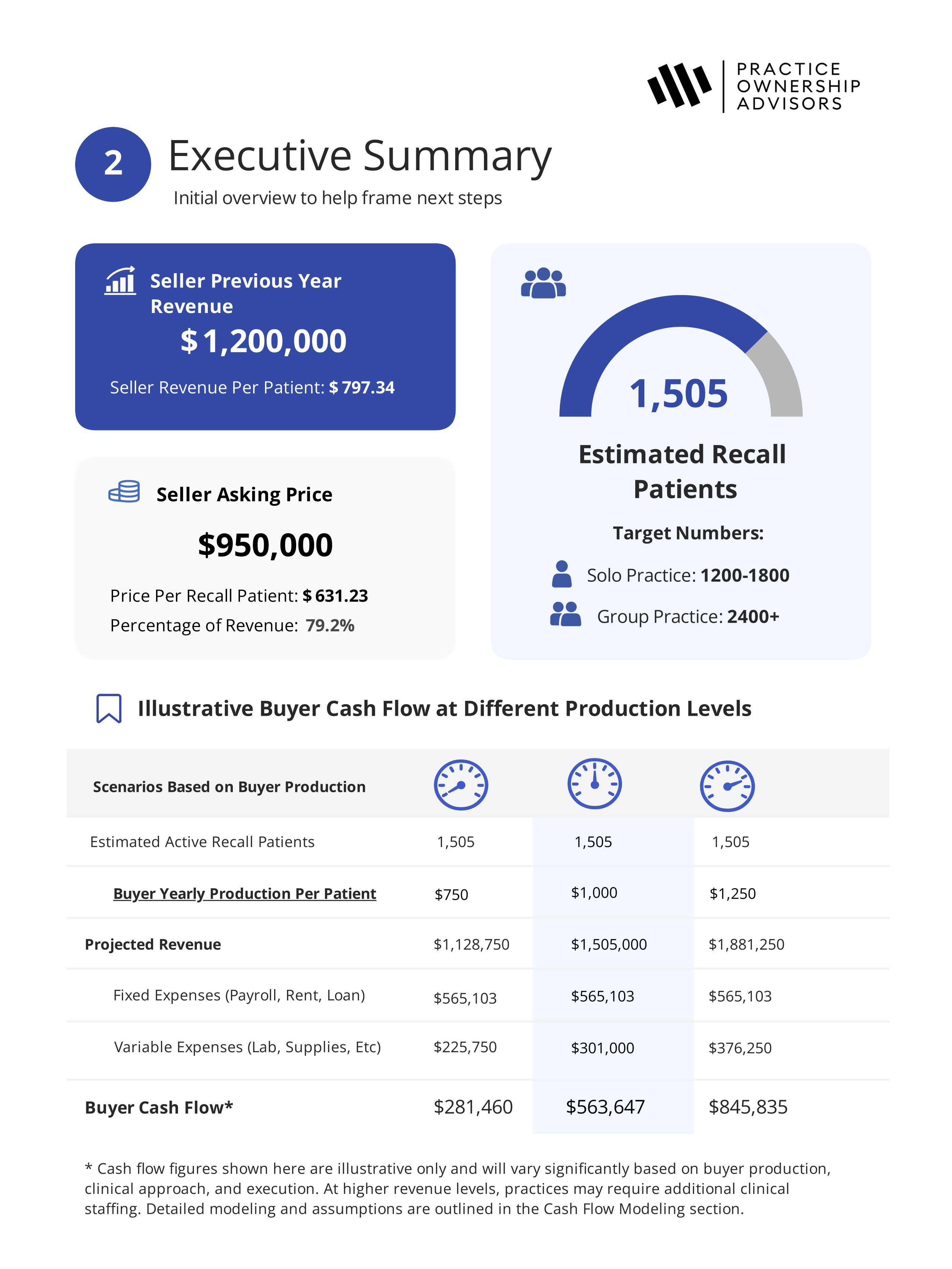

Your loan payment should be less than 12% of your projected revenue.

That's it. That's the rule. If you're buying a practice that does $1 million in annual revenue, your loan payment shouldn't exceed $120,000 per year. If it does, you're underwater before you even start.

Most practice loans are financed over 10 years at competitive rates. For a $500,000 practice, your annual loan payments will typically fall well under 12% of revenue, which is why most small practices are financeable.

But here's where people get in trouble: they overpay. They pay $700,000 for a $500,000 practice because a broker told them the valuation justifies it. Now their payment is $82,000-$92,000 per year. That's 16-18% of revenue. That's dangerous.

General Pricing Guidelines

Here's my framework for what to pay:

Don't pay more than 90-95% of the previous year's revenue. Simple rule. Practice did $800,000 last year? Don't pay more than $720,000-$760,000. This assumes the practice is healthy and stable.

Price per active recall patient: $500-$1,000. If the practice has 1,000 active recall patients, you're paying between $500,000-$1 million. This benchmarks the price against actual patient base rather than abstract revenue numbers.

Bank cap is typically 100% of revenue. Most banks won't lend more than the practice's annual production. Some practices trade above that, but those are usually cash deals or seller financing, and you need to be very careful.

Five Valuation Methods, Briefly

Brokers and accountants use different approaches. You should understand them, but don't let them override your affordability calculation.

Capitalization of earnings: Take the normalized income (money after expenses) and divide by a capitalization rate (usually 20-25%). This method can inflate prices when brokers creatively adjust the "normalized" income number by adding back owner perks and discretionary expenses to make the numerator bigger.

Asset-based valuation: Add up the tangible assets (equipment, supplies, leasehold improvements) and intangible assets (goodwill, patient base). This gives you a floor value but often understates what a practice is actually worth.

Percentage of annual revenue: Simply a percentage of last year's production (usually 60-100% of revenue). This is the bluntest tool but often the most realistic.

Comparable sales: Look at similar practices that sold recently in your market. This works in markets with good data. Most dental markets don't have reliable comps like real estate does.

Discounted cash flow: Project future revenue and discount it back to today's dollars. This is sophisticated but requires assumptions that are often wrong.

I won't lie: none of these methods are as standardized as real estate valuation. Dental practices don't trade like houses. There's no MLS. No standardized contracts. No transparency in pricing. Broker valuations often exist primarily to justify the asking price the seller wants.

Nine Factors That Actually Affect Value

Pricing isn't really about formulas. It's about what makes this specific practice more or less valuable than others.

Patient base stability: How long have patients been going there? High-value patients who've been there for years? That's worth more. New patients or high-patient-turnover? That's riskier.

Hygiene production: A practice with strong hygiene is more valuable than one where a single dentist does everything. Hygiene is more predictable and less dependent on one person.

Insurance mix: A practice with 75% private pay or PPO is worth more than one with 50% Medicaid and HMO. Reimbursement stability matters enormously.

Staff tenure and quality: Long-term staff who are competent and loyal add value. High turnover is a risk factor.

Facility condition and location: A nice location with modern equipment is worth more. An obsolete building in a declining neighborhood is worth less.

Debt and commitments: What's remaining on the lease? Are there equipment loans? These reduce the value available for the seller.

Growth trajectory: Is the practice growing, stable, or declining? Stability is good. Decline is risky. Growth can be risky if it's dependent on the current owner.

Regulatory or compliance issues: Have there been compliance problems? Insurance denials? Licensing issues? These create value risk.

Owner health and motivation: An owner burning out and disengaging is more likely to accept lower prices. A confident owner who could keep operating indefinitely can command more.

Why Broker Valuations Justify Inflated Prices

Here's what I've learned: brokers make commission on the sale price. The higher the price, the higher their commission. Conveniently, broker valuations often land at or above asking price. Coincidence? No.

A broker will add back "excessive" owner salaries, note location improvements, highlight recent equipment purchases, adjust for population growth. Before you know it, a practice that sold for $600,000 five years ago is suddenly worth $850,000.

Sometimes that's legitimate. Sometimes it's justification for an inflated asking price.

You want an independent accountant or your own analyst to evaluate the practice, not the broker's valuation. Pay them a fee. They're not invested in the sale price.

The Real Test

Can you afford the loan? Will the practice produce enough revenue to service the debt while you take a reasonable owner's salary? Will you have cash flow for operations, staff raises, equipment replacement, and building reserves?

If yes, the price is probably reasonable. If no, the price is too high, no matter what the valuation report says.

One More Point

Some sellers finance part of the deal (seller financing). That changes everything because the seller is betting on your success. It aligns incentives. You might pay the same total price, but if the seller is holding $200,000 of the financing, that's fundamentally different than a bank loan. You negotiate harder with an owner who's financially invested in your success.

Don't overpay because a formula says to. Pay what makes financial sense for your situation, what the banks will support, and what leaves you with genuine upside. Practice ownership should be a path to wealth, not a path to servicing debt.

Practice Evaluation & Advisory Service

Independent clinical and financial analysis to help you make an informed decision before you buy.

Learn more

Newsletter + Free Practice Evaluation Checklist

One actionable email per week on buying the right practice, plus an instant download of our free Practice Evaluation Checklist.

One email per week. Checklist delivered instantly. Unsubscribe anytime.