Insurance credentialing is the hidden bottleneck after buying a practice. Learn when to start, which insurances matter most, and why the insurance mix determines your actual revenue.

You're going to close on your practice on a Friday. Monday morning you're going to see patients. By Thursday, insurance denials are going to start rolling in. You're going to call the insurance company and they're going to tell you that you're not credentialed.

This is the most common surprise that hits new practice owners, and it's entirely preventable.

Start Credentialing Before Closing

This isn't negotiable. Start the credentialing process at least 60 days before closing. Some insurances process in 30 days. Others take 90. You don't have time to learn this lesson the hard way.

Delta Dental is usually fastest, typically 30-45 days. United Healthcare can be 60 days. Some smaller, regional plans take 90-120 days. Medicaid varies by state but often takes longer than commercial plans.

The time to start is when your purchase agreement is signed, not when the money changes hands.

Two Credentialing Approaches

You have a choice: strict credentialing or credentialing with rate negotiation.

Credentialing only: Get yourself credentialed as the owner/provider with insurances at the rates they're already paying the practice. This is the fastest path. You get live in 30-60 days. It's the right move if you want to get up and running quickly.

Credentialing plus rate negotiation: At the same time you're credentialing, you negotiate higher reimbursement rates. This is slower and more complex. You need contracts returned, reviewed, signed, and resubmitted. This adds 30-60 days to the process.

My advice: credential first, negotiate later. Get live and generating revenue. Once you're established and have a track record, you can renegotiate. The rate improvement won't justify months of missing revenue.

The Tools You Need

CAQH profile: CAQH (Council for Affordable Quality Healthcare) is the universal credentialing database that most major insurers pull from. Every provider needs one. You'll use this for most credentialing applications. Build it out completely and accurately because you'll reference it constantly.

DentalXChange: This is used by Delta Dental and some other carriers for credentialing. It can be faster than individual applications for the plans that accept it.

Individual insurance applications: Some smaller plans require their own application forms. Collect these early.

Get your NPI number from NPPES before you close. You're going to need it constantly.

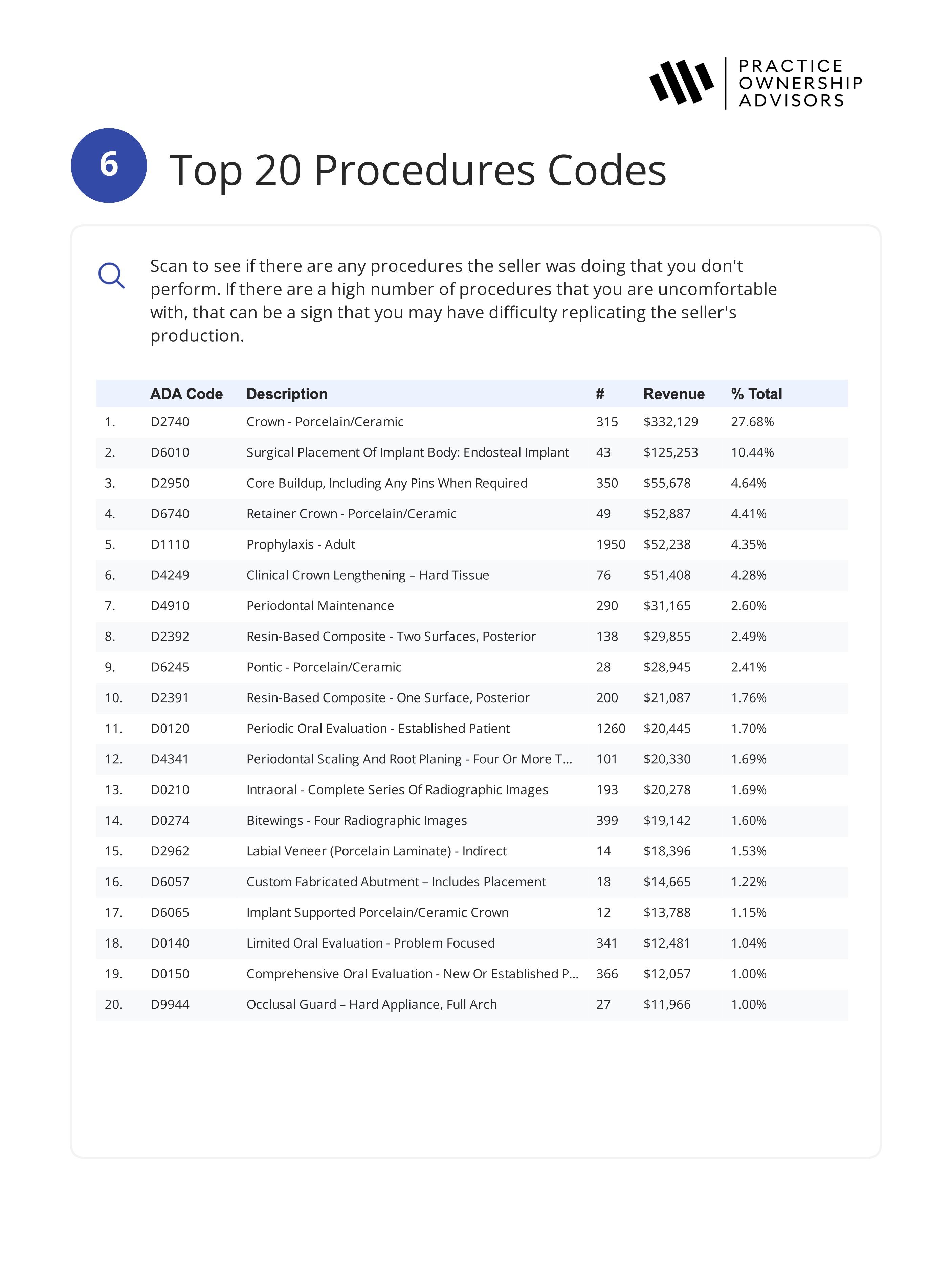

The Insurance Mix That Actually Matters

Not all insurance is created equal. Where your patients come from determines your actual revenue, not your gross production.

Cash and fee-for-service (FFS): Highest reimbursement. You set the price. No insurance company negotiating what you get paid. But patient acquisition is harder and patient attrition risk is higher. People drop cash care faster than insurance care if they change jobs or get tight on money.

PPO (Preferred Provider Organization): Sweet spot. Good reimbursement, patient volume, and retention. PPO patients stay because they're used to insurance coverage. If they stay employed, they stay as patients. This is the goldilocks insurance type.

HMO (Health Maintenance Organization): Lower reimbursement. Required by contract to accept their reimbursement rates and fee schedules. High utilization (patients use benefits) but very tight margins. The capitated HMO plans are the worst because you get a flat fee per patient regardless of treatment needed.

Medicaid: High volume, very low reimbursement. Some practices build around Medicaid volume because there's a lot of it, but margins are razor-thin. Good if you're specialized in high-volume, low-complexity dentistry.

What I Actually Recommend

My ideal insurance mix for a general practice buyer: 50-75% PPO, 25% cash, and minimal HMO or Medicaid.

Why? PPO patients are sticky. They're stable. Reimbursement is predictable. You can build a business around PPO volume. Cash patients give you margin but require more acquisition and retention effort. HMO and Medicaid plans pay poorly and add administrative burden, so you want to be very careful about how much of your revenue depends on them.

Look at the practice you're buying. What's their insurance breakdown? If it's 40% Medicaid and 20% HMO, you're inheriting a revenue model that's going to be hard to fix. That affects valuation. If it's 70% PPO, you're buying something much more valuable.

Critical Warnings About Insurance

Out-of-network checks: When patients are covered by insurance but you're not contracted with that insurance, the insurer often sends the check to the patient, not you. You're chasing patient reimbursement instead of getting paid directly. This is cash flow disaster. Know which insurances cover the practice and stay on top of credentialing so you don't end up as out-of-network.

Billing under the seller's NPI: This is a critical issue. If the seller was an individual provider with their own NPI, you can't just use their NPI to submit claims. You need to be credentialed individually. If you keep billing under their NPI, those claims don't belong to you. The insurance company will deny them when they realize the treating provider and the billing provider don't match. Get your own NPI established before closing.

Contracts and termination: When you buy the practice, you technically inherit the contracts, but you need your own credentials under your NPI. Some insurances require a new agreement when the provider changes. Others grandfather existing contracts. Know what you're inheriting and what you need to replace.

Prior authorizations: Understand which insurances require prior authorization for procedures. Running expensive treatment without authorization is a quick way to get unpaid claims. This information varies by plan and is complex, but it's essential.

Timeline for Credentialing

Day 1: Get your CAQH profile complete and your NPI number.

Day 5-10: Identify all the insurances that the practice is contracted with. Ask the seller or the billing department for a complete list.

Day 10-30: Start applications with major insurances. Use DentalXChange when possible.

Day 30-60: Follow up on applications. Track the status. Expect requests for additional information.

Day 60-90: Most major insurances should be credentialed. Continue pursuing slower plans.

Day 90+: By the time you close, you should be credentialed with at least 80% of the insurances the practice is on. Some stragglers will still be processing.

After closing: Continue pursuing credentials for the remaining plans.

The Real Impact on Revenue

Insurance credentialing isn't an administrative detail. It directly determines how fast you can bill patients, when you get paid, and whether you're paid at all.

A practice that can't bill for 60 days after closing loses money. A practice that's improperly credentialed (billing under the wrong NPI) loses claims and revenue. A practice with the wrong insurance mix (high HMO, high Medicaid, lots of out-of-network) has fundamentally lower income than the production numbers suggest.

Get credentialing right and it's invisible. Get it wrong and it's a disaster.

Practice Evaluation & Advisory Service

Independent clinical and financial analysis to help you make an informed decision before you buy.

Learn more

Newsletter + Free Practice Evaluation Checklist

One actionable email per week on buying the right practice, plus an instant download of our free Practice Evaluation Checklist.

One email per week. Checklist delivered instantly. Unsubscribe anytime.